The phrase “fog of war” refers to the uncertainty, confusion and lack of situational awareness that military commanders experience during conflict.

Decisions must be made with incomplete information, often leading to unexpected outcomes.

While the recent conflict involving Iran appears to have reached a fragile conclusion, it could be argued that financial markets have been operating in their own fog of war throughout the crisis.

When hostilities escalated at the end of February, oil prices surged by almost 80 per cent as markets quickly priced in disruptions to Middle Eastern energy supplies.

The sharp rise sparked widespread concerns about a new wave of inflation, higher interest rates and the possibility of a global economic slowdown.

The conventional market narrative seemed straightforward: higher energy prices would push inflation higher, central banks would be forced to keep interest rates elevated, and risk assets would come under pressure.

Market commentators strongly anticipated a prolonged era of elevated oil prices due to the massive supply shocks caused by the complete closure of the critical Strait of Hormuz waterway. During the peak of the conflict, energy experts and major financial institutions warned that crude could remain locked in a high range for years.

Yet that is not what happened.

Oil prices have now largely retraced their gains, with Brent crude returning to levels seen before the conflict began. Instead of the shortages many feared, parts of the oil market now have plenty of supply, leading to renewed weakness in prices.

Equally surprising has been the behaviour of technology stocks.

Traditionally, high-growth technology companies are among the most sensitive sectors to rising interest rates because a large portion of their value is derived from future earnings. As bond yields initially climbed and inflation fears intensified, many investors expected technology shares to struggle.

Instead, the opposite occurred.

The Nasdaq index - primary benchmark for technology and growth-focused companies - has continued its relentless advance, reaching new highs despite the uncertainty surrounding inflation, interest rates and geopolitical tensions. Much of this enthusiasm has been driven by investor excitement surrounding artificial intelligence.

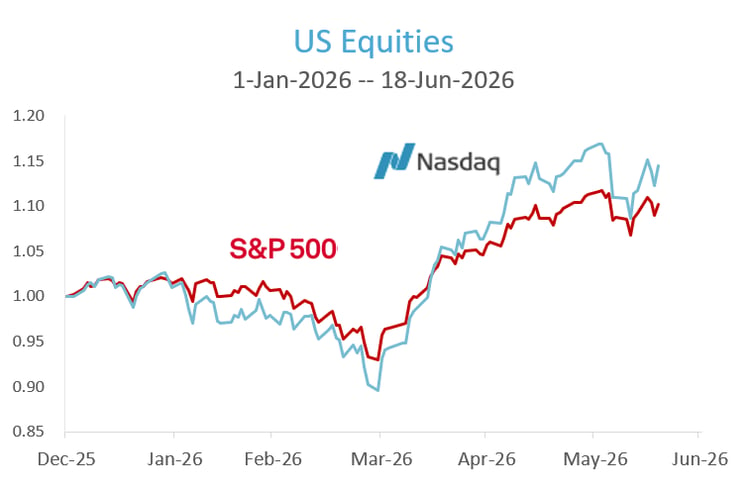

The chart below shows that the Nasdaq index is up over 17% since the conflict began (and despite the dip on the initial outbreak of hostilities the Nasdaq is up 14.5% since the start of the year). The broader US market as represented by the S&P 500 Index is not far behind as it is up just over 10% since the start of the year.

Source: investing.com, S&P 500 total return index, Nasdaq composite total return index

What’s more impressive are Asian technology stocks – they are up 65% since early March, after being flat for the first part of the year. These stocks have been driven by the explosive global Artificial Intelligence investment boom.

Taiwan and Korean semiconductor heavyweights like Samsung Electronics and SK Hynix have benefited tremendously from surging demand for memory chips, while firms like TSMC provide crucial manufacturing for global AI processor.

Source: investing.com, Betashares Asia Technology Tigers ETF (ASX: ASIA)

There is little doubt that artificial intelligence represents a transformative technological development. The potential applications across industries are vast and could reshape the global economy over the coming decades.

However, history reminds us that transformative technologies do not always translate into attractive investments at any price.

Investors appear willing to overlook questions about whether the enormous capital expenditure currently being poured into AI infrastructure will ultimately generate sufficient returns. The benefits may indeed be substantial, but the scale of investment required is also unprecedented.

Gold has provided another surprise. Traditionally viewed as a hedge against inflation, geopolitical instability and financial uncertainty, many expected gold prices to surge as the conflict escalated. Instead, gold prices have drifted lower.

The chart below shows the Dow Jones Commodity Gold Index. The index is down 19% since the start of the war in late February and is now below where it started at the start of the year.

Part of the explanation for this downward slide may lie in shifting expectations around inflation and interest rates.

When oil prices spiked at the start of the year, so did bond yields in expectation of higher inflation and higher interest rates. But instead of hedging against inflation, investors have swapped out of gold into higher-interest paying bonds. As gold also produces no income, it becomes less attractive when investors believe real returns can be earned elsewhere.

As oil prices retreated and fears of prolonged supply disruptions eased, investors have become less concerned about a sustained inflation shock, further weakening the attraction of gold. While gold can provide diversification benefits and protection during periods of extreme uncertainty, it can also be volatile and may underperform for extended periods.

Taken together, these developments suggest that markets have not behaved in the rational manner many expected during a period of war, inflation concerns and slowing economic growth. Have financial markets been operating in a fog?

Summary

History teaches us that wars often create a “fog” that obscures reality. Military leaders use the term to describe the uncertainty that surrounds a battlefield. Information is incomplete, outcomes are unknowable, and threats are often hidden until they suddenly emerge. Financial markets can experience a similar phenomenon. Investors become focused on visible developments while overlooking risks that are less immediate but potentially more damaging.

Or perhaps this is simply another reminder that economic logic and market behaviour are not always closely linked in the short term. Markets are driven by countless factors, including sentiment, expectations and investor positioning. Even when the economic outlook appears obvious, markets can chart a very different course.

As the economist John Maynard Keynes famously observed:

“The markets can remain irrational longer than you can remain liquid.”

For investors, the lesson is not to predict every market twist and turn.

Instead, it is to remain disciplined, maintain a diversified portfolio and stay focused on long-term objectives. Markets will always surprise us. A well-constructed investment strategy is designed to withstand exactly that.

This article was written by Dr Steve Garth - Principal of Principia Investment Consultants.

The information provided is factual only and does not constitute financial advice. If you need to speak with a Financial Adviser before making a decision, you can contact us via the button below.

Leave a Comment